All Categories

Featured

Table of Contents

There is no payment if the plan runs out prior to your fatality or you live past the policy term. You may be able to restore a term plan at expiration, yet the premiums will be recalculated based on your age at the time of revival.

At age 50, the premium would certainly rise to $67 a month. Term Life Insurance Policy Fees 30 years old $18 $15 40 years old $28 $23 half a century old $67 $51 Source: Quotacy. Quotes are for a $250,000 30-year term life plan, for males and females in exceptional health and wellness. In contrast, here's a consider rates for a $100,000 entire life policy (which is a sort of irreversible plan, meaning it lasts your life time and consists of cash value).

Interest rates, the financials of the insurance company, and state laws can also impact premiums. When you think about the quantity of protection you can get for your premium dollars, term life insurance coverage has a tendency to be the least costly life insurance.

Thirty-year-old George intends to shield his family members in the not likely event of his passing. He acquires a 10-year, $500,000 term life insurance plan with a costs of $50 per month. If George passes away within the 10-year term, the policy will pay George's recipient $500,000. If he passes away after the policy has run out, his recipient will certainly obtain no benefit.

If George is identified with a terminal disease throughout the initial policy term, he probably will not be eligible to renew the policy when it expires. Some policies use guaranteed re-insurability (without proof of insurability), but such attributes come at a greater expense. There are several sorts of term life insurance coverage.

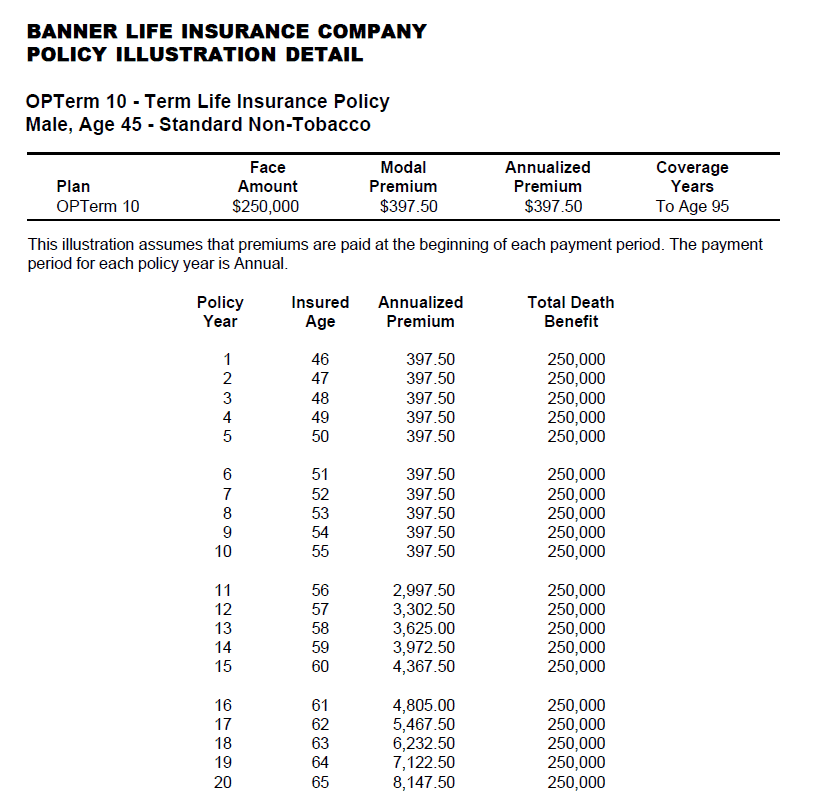

Normally, many firms supply terms ranging from 10 to thirty years, although a few offer 35- and 40-year terms. Level-premium insurance has a set monthly payment for the life of the plan. A lot of term life insurance policy has a degree costs, and it's the type we have actually been referring to in a lot of this post.

Tax-Free A Whole Life Policy Option Where Extended Term Insurance Is Selected Is Called

Term life insurance policy is attractive to young people with kids. Parents can acquire considerable insurance coverage for an inexpensive, and if the insured dies while the policy is in result, the family can count on the survivor benefit to replace lost income. These policies are also fit for individuals with growing family members.

Term life plans are ideal for people that want substantial protection at a reduced expense. People that possess whole life insurance coverage pay a lot more in premiums for much less protection yet have the protection of knowing they are secured for life.

The conversion cyclist should permit you to transform to any irreversible policy the insurer supplies without restrictions. The key attributes of the motorcyclist are maintaining the initial health and wellness score of the term policy upon conversion (even if you later have health and wellness problems or end up being uninsurable) and making a decision when and just how much of the coverage to convert.

Of course, overall premiums will enhance substantially considering that entire life insurance policy is a lot more pricey than term life insurance coverage. The advantage is the guaranteed authorization without a medical examination. Clinical conditions that develop throughout the term life duration can not cause costs to be boosted. However, the firm may need restricted or complete underwriting if you want to include additional riders to the new policy, such as a long-term care cyclist.

Whole life insurance policy comes with considerably higher month-to-month premiums. It is suggested to provide insurance coverage for as long as you live.

Expert Guaranteed Issue Term Life Insurance

It depends on their age. Insurance firms established an optimum age limit for term life insurance policy plans. This is generally 80 to 90 years of ages yet may be greater or lower depending on the firm. The premium additionally increases with age, so a person aged 60 or 70 will certainly pay substantially greater than someone decades more youthful.

Term life is somewhat comparable to auto insurance coverage. It's statistically not likely that you'll require it, and the premiums are cash down the tubes if you do not. Yet if the worst takes place, your family will obtain the benefits.

The most prominent kind is currently 20-year term. The majority of companies will not market term insurance policy to a candidate for a term that finishes past his or her 80th birthday celebration. If a plan is "eco-friendly," that means it continues in pressure for an extra term or terms, up to a specified age, also if the health of the insured (or other elements) would trigger him or her to be rejected if she or he looked for a brand-new life insurance plan.

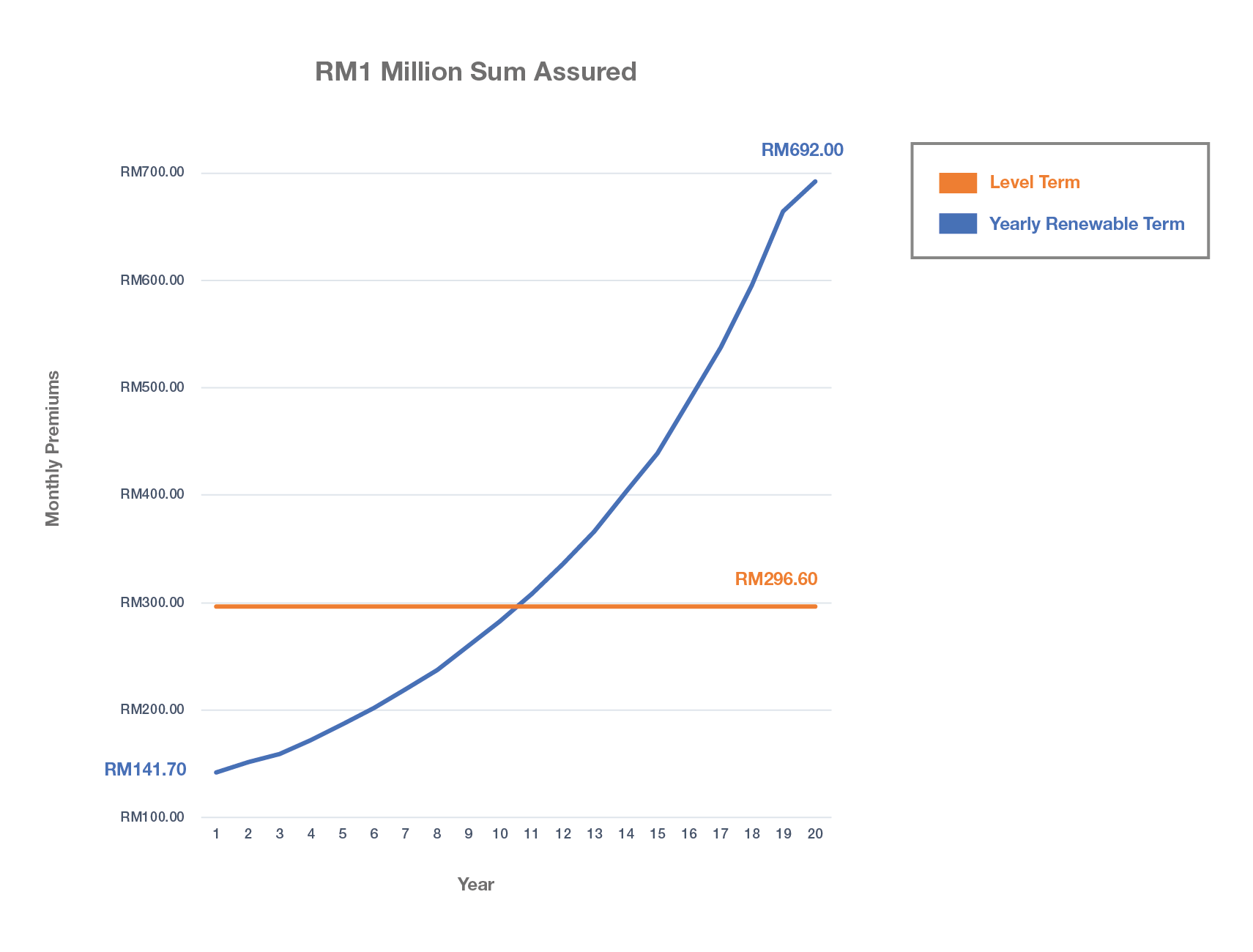

So, premiums for 5-year renewable term can be level for 5 years, after that to a new price reflecting the new age of the insured, and so on every 5 years. Some longer term plans will guarantee that the costs will certainly not boost throughout the term; others do not make that guarantee, allowing the insurance provider to increase the rate throughout the plan's term.

This means that the plan's owner can transform it right into a permanent kind of life insurance policy without additional evidence of insurability. In many kinds of term insurance policy, including homeowners and auto insurance coverage, if you haven't had a case under the plan by the time it ends, you obtain no refund of the premium.

Quality Annual Renewable Term Life Insurance

Some term life insurance coverage customers have actually been dissatisfied at this result, so some insurance firms have actually produced term life with a "return of costs" feature. guaranteed issue term life insurance. The costs for the insurance policy with this feature are frequently dramatically more than for policies without it, and they generally call for that you maintain the policy effective to its term or else you waive the return of premium benefit

Level term life insurance coverage premiums and survivor benefit stay regular throughout the plan term. Level term plans can last for durations such as 10, 15, 20 or thirty years. Degree term life insurance policy is usually extra cost effective as it doesn't construct cash money worth. Degree term life insurance policy is among one of the most usual sorts of protection.

Top A Term Life Insurance Policy Matures

While the names commonly are used interchangeably, level term coverage has some vital distinctions: the costs and survivor benefit remain the same throughout of insurance coverage. Level term is a life insurance policy plan where the life insurance policy premium and death advantage stay the very same for the duration of insurance coverage.

{kind=link}

Latest Posts

Funeral Expense Insurance Policy

Compare Funeral Insurance

Is Funeral Insurance Worth It